401k is a potent tool, which is an employer-sponsored retirement saving plan that provides a feature of saving by withdrawing some money from their monthly salaries and saving in a continuously growing account, like, 401k. So, let’s deeply understand “what is a 401k”.

Understanding 401k

As mentioned before, a 401(k) is a savings account offered by the employer to employees. The amount contributed to a 401(k) account is pre-tax, which means the amount going into this account is calculated before the taxes on your monthly salary.

Sometimes this contribution can be from both side employee and the employer. These contributions are usually invested in mutual funds, stocks, bonds, or target-date funds. The types of 401(k) account are:

Traditional 401(k)

This is the traditional 401 (k) account in which the contribution is made from pre-tax income. This means the salary amount before taxes is divided into a small portion, which goes to the savings account. This reduces your taxable income and provides immediate tax savings. But the taxes are paid at the time of withdrawal from the account after retirement.

Roth 401(k)

In this type of saving account, the deposit is made after the tax means no tax will be applied from now, but qualified withdrawals in retirement are tax-free.

Both accounts have their scope of advantages, you can choose the best fit plan based on your requirements and budget.

Want to see how much your 401(k) could grow? Try our easy-to-use 401(k) calculator and plan your retirement with confidence!

How Does A 401k Work?

The working of a 401(k) account is very simple and clear. When you enrolled in the 401(k) savings plan. You chose a portion of your salary that would be contributed to the 401(k) savings plan. After that, you must choose an investment policy or plan, and the account starts.

Afterwards, as time passes, the money in the 401(k) starts to increase by two modes: one is your contribution, and the other is the interest or profit on the amount you are depositing in the savings account.

Eligibility For Enrolling In 401k

Qualifying for having a 401(k) savings account is easy, but there are some criteria to be fulfilled. Which are :-

- Employment Status : You need to be employed in a company that offers a 401(k) account.

- Minimum Age : You must be at least 21 years old to qualify for a 401(k).

- Service Requirement : The applicant must be employed for at least 1 year.

- Employer Matches : There is a criterion to qualify for taking advantage of the employer matches system.

- Enrollment Period : You can typically join the plan during open enrollment or upon hiring, based on company policy.

Benefits of 401k

What is a 401 (k)? So, 401(k) is one of the most beneficial savings options offered by the employer for the sake of employees in their retirement time.

Also, it has numerous numbers of advantages which make it an ideal choice for depositing and increasing money with time. Benefits are :-

- Tax advantages (pre-tax contributions or tax-free withdrawals)

- Employer Matching Contributions : The employers will invest their money with your money, which leads to higher returns and reliable growth.

- Automatic Payroll Deductions : After your successful enrolment, you don’t need to deposit money; automatically, the amount will be deducted from your monthly paychecks.

- Compound Growth Over Time : You can view constant growth over time.

- Higher Contribution Limits Compared To IRAs : As compared to the Retirement Account, a 401(k) offers higher annual contribution limits that an employer can deposit.

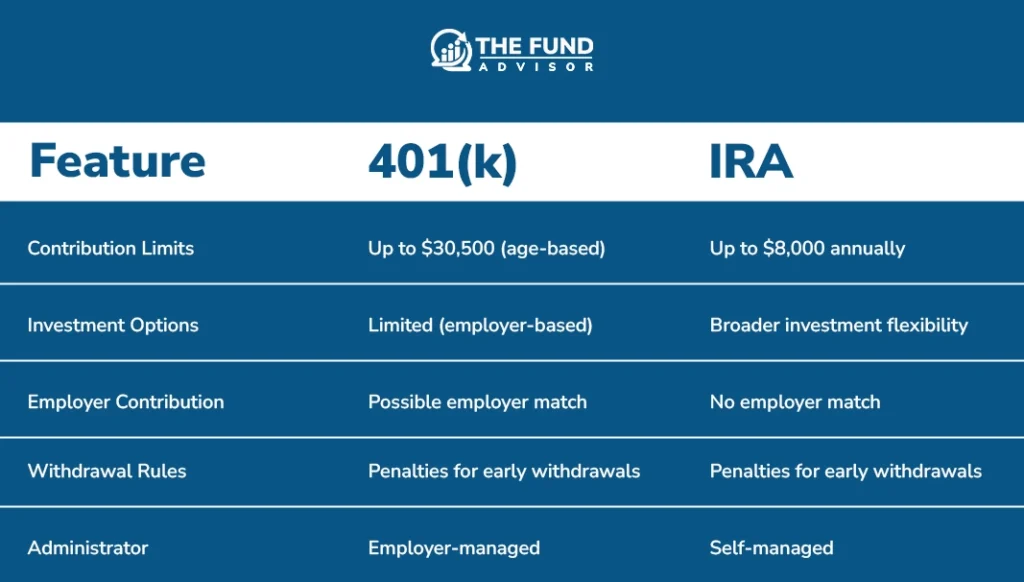

How 401k Plans Compare With IRAs?

What is a 401k enclosing the comparison of 401(k) with an Individual Retirement Account (IRA). While both provide tax advantages, the are many significant differences present in both the savings account options which can be chosen based on the needs and future goals of the employees:

- Contribution Limits : Interestingly, 401(k) plans provide higher annual contribution limits than IRAs. In 2025, you can contribute between $23,000 to $30,500, based on age, in a 401(k) account. Whereas in the IRA, you can only contribute up to $8000 annually.

- Investment Options : Generally, an IRA offers a larger scope of investment options than a 401(k), which is limited to the employer only. With an IRA, the investor can get more control and flexibility over their money.

- Employer Contribution : One of the most significant advantages of a 401(k) is that it has an option for the employer to match the contribution amount. Meaning the employee can get higher returns and free money at the time of retirement.

- Withdrawal : Both accounts charge penalties and fines for early withdrawal of money. And have an age limit after which no penalty will be applied.

- Administrator : 401(k) accounts are generally managed and administered by the employer; the complete contribution and investment are made by the employer itself. In the IRA, the individual or the account holder is the single owner of the account and is responsible for opening and maintaining the account.

To make the most of your 401k, it’s important to know When is the best time to start saving for Retirement.

How Much Should I Contribute and How Much Can I Save?

It is advised to contribute at least 15% of your pre-tax income annually for retirement. This includes contributions and employer contributions. This threshold is defined as an ideal contribution level.

If you’re a new employee or didn’t have that much margin of contribution. It becomes essential to understand what is a 401k? After this, you can start with a lower percentage like 5% annually and then increase this percentage by 1% each year till you exceed the 15% ideal level.

For 2025, the IRS allows employees under 50 to contribute up to $23,000 to a 401k. These limits apply only to the individual account; if the employers have an option of employer match contributions, then the amount can be higher. If you are taking any loan on your 401(k) account, then you need to understand, will my employer know if I take a 401(k) loan.

If you’re young and have low daily expenses, such as unmarried or solo expenses, then try to contribute as much as you can to maximize the retirement benefits with much higher returns on the investments and savings. With this approach, you can easily tell anyone who asks what is a 401k savings account.

How Much Should I Have In My 401k? Setting Retirement Benchmarks

Saving for retirement is not only understood by the contribution amount, but also requires knowing how much you should have in your 401(k) at a certain age. See what the expert says : –

- By age 30 : 1x your annual salary

- By age 40 : 3x your annual salary

- By age 50 : 6x your annual salary

- By age 60 : 8x your annual salary

- By age 67 : 10x your annual salary

These are the general milestones advised to follow, but not necessary to achieve. Based on your budget and monthly expenses, you can choose the best contribution plan. Using our 401k calculator, you can easily calculate savings over time with a one-step process and get the complete insight into what a 401k is.

If you’re in your late 20s, it’s worth knowing how much should you have in 401k by 30 to stay financially prepared.

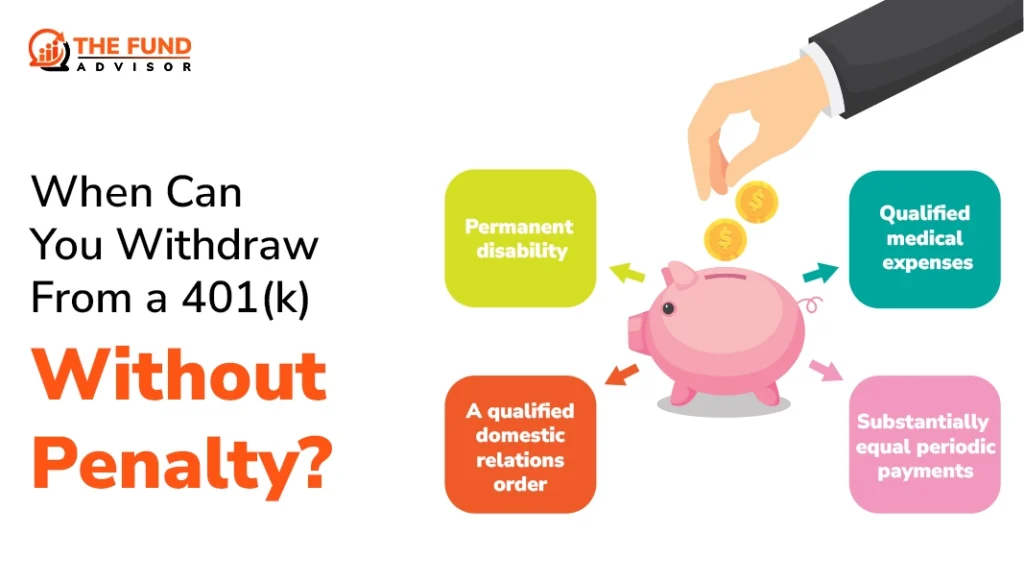

When Can You Withdraw From A 401k Without Penalty?

As we have quite a good knowledge of what is a 401k, we are proceeding further. Generally, if you want to withdraw funds from your 401(k) account without penalty, it is possible after the age of 59½ years; withdrawing before this age can result in a 10% penalty with the usual taxation applied.

There are some exceptions where you can withdraw early without penalty, such as : –

- Permanent disability

- Qualified medical expenses

- A qualified domestic relations order (QDRO)

- Substantially equal periodic payments (SEPPs)

Also, if you leave your job after 55 or more, then you can withdraw from your 401 (k) account early without penalty. This is called rule 55. Know how to withdraw money from 401(k) before retirement.

How To Take Money Out of 401k?

There are various ways available to withdraw money from your 401(k) account :-

- Direct Withdrawal : This is the most basic way to withdraw. In this, you can withdraw money directly from your savings account after the desired age to prevent any penalty and fines. If you withdraw early, which is possible, but you will face penalties, usually of 10%.

- Loans : This is a popular way in which you can take a loan over your 401(k) savings account, which will be paid (usually over 5 years) with an interest mentioned in the loan document. You can take a loan up to 50% of the vested amount in your 401 (k) account. In the case of leaving, he job with an outstanding loan can cause penalties and fines.

- 401(k) Rollover : This means if you leave your present job, then you can rollover over or transfer the current 401(k) plan to another savings plan in a different organization.

- IRA Rollover: You can rollover your 401(k) funds to an Individual retirement saving accout or an IRA, which gives more flexibility and control over your money. Click to know the difference of Roth IRA and 401(k).

So, if you’re wondering that “Can I withdraw from my 401k?” -the answer is yes, but before withdrawing, you need to know the fines and penalty focus.

How To Check Your 401k Balance?

Monitoring your 401(k) account is an essential part of planning for retirement. With timely analyzing the growth and contribution limits you can easily save a well saved of money.

Nowadays, most employers have a simple online portal to view the savings and contributions. You can easily log in with some credentials to see the stats. On the 401(k) dashboard, you can monitor current balance, contribution amount, analyse investment performance, and review any employer matching contributions.

In addition, many plan administrators provide monthly or timely based email services by sending the complete statement via email. If you didn’t know what is a 401k account is and how to use all these features, then contact your HR department.

How Much In Your 401k To Get $1,000 A Month?

Using the 4% safe withdrawal rate, you can estimate how much you need to save to generate a monthly income.

$1,000 × 12 = $12,000 annually

$ 12000/0.04 = $300,000

You’d need approximately $300,000 saved in your 401(k) to safely withdraw $1,000 a month. You can use our 401 (k) calculator to break down the numbers in an easy way.

Common Mistakes To Avoid In Managing 401k

Some mistakes are there that prevent an employee from getting the maximum benefits from their 401(k) savings account.

The mistakes are :-

Irregular Monitoring The 401(k) Account

Many people forgot to monitor and review their 401(k) through online portals, which results in unexpected losses or penalties due lack of attention to growth.

Ignoring Investment Charges

Mutual fund investments can be chargeable means the invested money has to pay some processing or platform fees. And low returns with high fees can lead to losses in investment.

Failing To Increase Contribution

As time passes and your seniority level increases, your annual income also increases. It is important to increase the contribution amount annually to get higher returns.

Not Taking Full Advantages of Employer Match

If you’re not aware of the scope of advantages or what is a 401(k) in real life, then you cannot achieve the maximum potential that can be achieved with a simple understanding.

Conclusion :-

When the concern for having a retirement savings arises, one of the most famous ways is 401k retirement saving accounts. This is specifically designed to faciliate the money saving option. With monthly contributions and return of investment features, this cecomes an idela chlice for individuals who are seeking a decent retirement savings.

401k savings accounts come with various advantages like tax advantage, growing money, higher retirement income, higher contribution, and saving limits. Generally, it is advised to contribute at least 15% of your annual income. WIth this you can get enough retirement benefits and savings to live with peace and confidence.

If we talk about withdrawal from a 401k account is possible or not. Then the answer is it is possible, but with some penalties and fees. Withdrawing money before the age of 59½ years will result in a 10% penalty, and after this age, no penalty will be applicable.

You need to monitor your savings and growth on the online portal provided by the employer, which can be accessed using the credentials given to you. So, we talk about what a 401 (k) is or how much you should have in it? This guide will be a one-stop solution for all of this.

Please follows us if you like this article and share it with your family and friends.

Frequently Asked Questions

What is a 401 (k) and how does it work?

It is an employer-sponsored investment savings account that is offered to employees, and a portion of the employee’s monthly salary will go to this account and grow with time, and can be accessed after retirement.

What are the 3 benefits of a 401 (k)?

While 401k has many benefits, some of which are tax advantages, money grows as the money is invested by the employer in the mutual funds or various investment systems, and employer matches provide free retirement money.

Can I withdraw my 401 (k)?

Yes, you can withdraw money from the 401k savings account after the age of 59½. Early withdrawal penalty of 10% with the general taxation applied to it. You can withdraw by taking a direct withdrawal (Penalty applicable), loan on the 401 (k) account, and rolling over the plan into another plan when you leave your current job.

How is a 401 (k) taxed?

401k is of two type traditional 401k and Roth 401k. In a traditional 401 (k), the contribution amount is pre-taxed, and the tax will be applicable at the time of withdrawal after retirement. In Roth 401k, the contribution made is after tax deduction, so usually no tax is applicable during the withdrawal after retirement.

What happens to my 401k if I quit my job?

If you quit your current job and have a savings account like a 401 (k), then there are various ways to manage this situation. You can cash out from the account, which charges a 10% penalty, or rollover the plan into an individual retirement account (IRA), or rollover the current 401 (k) account to the new employer’s 401 (k) account plan.

What is the 401k limit for 2025?

The contribution limits of 401k or any other retirement savings vary with time. In 2025, you can contribute between $23,000 to $30,500 in a 401k savings account.